Changes in the supply and demand in the private rented sector (PRS) has been growing for at least the last couple of decades, due to a number of long-term trends which have contributed to this; for example the limited availability in social housing, the increase in the cost of owner-occupation, changes in lifestyle, such as young households settling down later and the rise in one-person households. This has contributed to the landscape of the housing market changing and there are now a plethora of investment options for landlords, which no longer entails choosing the traditional options of the buy-to-let. Many people can’t afford to rent on their own or even dream about buying a property, so they have turned to shared accommodation instead and to cash in on this growing demand, landlords are converting old family homes into houses in multiple occupation (HMOs), as well as student accommodation being a sought after investment.

The rise of HMOs

It was in 2004 when, the Housing Act introduced licensing for houses in multiple occupations (HMOs) and most of the act came into force on 6th April 2006, except for sections relating to converted blocks of flats. According to the charity Shelter, an HMO could be a house split into separate bedsits, a shared house or flat, where the sharers are not members of the same family, a hostel, a bed-and breakfast hotel that is not just for holidays and a shared accommodation for students – although many halls of residence and other types of student accommodation owned by educational establishments are not classed as HMOs. HMOs are usually rented out by at least 3 people who are not from 1 ‘household’ (for example a family) but share facilities like the bathroom and kitchen. Typically rented by young adults or students, but they are by no means limited to these brackets. Earlier this year, The Guardian released figures showing that people in their mid-30s and 40s are now three times more likely to be renting compared to 20 years ago. It’s no surprise to the see the demand from tenants soaring.

HMOs have increased in popularity over the decades, both for landlords and for tenants seeking somewhere to live. This has been predominately driven by the great recession in 2008, which is often referred to as the economic downturn, where the global credit crunch led to a prolonged period of low/negative growth, rising unemployment and a period of fiscal austerity.

The primary cause of the great recession was of course due to the global banking system becoming short of funds, which then led to a decline in confidence and a decline in bank lending.

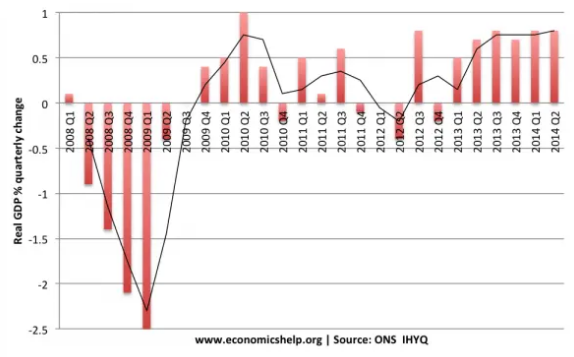

In particular, the great recession highlighted problems within the Eurozone, which experienced a double-dip recession and high unemployment, and from the graph below you can see the sharp fall in real GDP in the UK economy in 2008 and 2009 and it was also the slowest recovery on record.

UK economic growth

(Source: Office for National Statistics IHYQ)

The recession helped to pave a new path in the housing market

Despite the economic downturn of the recession, it helped to pave a new trend in the housing market, whereby landlords became increasingly focused on choosing to grow their residential property portfolios by taking on House in Multiple Occupation (HMOs), as well as flocking to the student accommodation sector, rather than focusing on more productive property sectors like homebuilding.

According to the charity Shelter, change in supply and demand, in the private rented sector has been growing in recent years and there are a plethora of long-term trends which has contributed to this; for example, the limited availability of social housing, the increase in the cost of owner-occupation, changes in lifestyle such as young households settling down later and the rise in one-person households.

As well as this conventional property price growth faltered due to borrowing restrictions, lower employment, lower incomes and reduced demand, the various statutory bodies responsible for housing our huge and growing student populations soldiered on with public spending budgets set in stone and guaranteed occupant uptake. This has all been the catalyst for the HMO market, which has now become a safe haven for investors in uncertain times.

HMOs in demand despite the pandemic

Since the 2020 pandemic, we are now living in a time where house prices are rising; mainstream lender’s criteria are tightening and finding a mortgage offer with a 10% deposit is near to impossible. Yet renting has never been so popular and Houses of Multiple Occupancy (HMO) are becoming well sought after. With demand for rental property on the rise, HMOs are becoming an attractive opportunity. Landlords can benefit from a regular income, but also potentially enjoy growth in the value of the property.

Housing with direct transport links to London are always more expensive than the UK average. HMOs in these areas are usually highly desired by commuters, as they often cannot afford to purchase these properties.

Cities such as Birmingham, Leeds, Liverpool, Newcastle, Sheffield all fit the bill for HMO landlords looking for a way to make their next profitable move. The trend for the size of a typical household in the UK is declining, whilst at the sane time, the population is increasing, leading to an increase in demand for HMOs and opportunities for buy – to -let landlords.

So why are they becoming such a desirable opportunity?

Rental yields are higher compared to traditional buy-to-let investments and currently in high demand among renters, including student, young professionals and families. A specialist property accountant Stephen Fay ACA, states he “often sees gross rental yields of 12-15% achieved, with some investors hitting 20% – plus (typical single-let property yields around 6-7%).”

Despite the pandemic causing considerable damage globally, there were still reasons for people to invest in HMOs. The first one being the stamp duty holiday, which Rishi Sunak introduced. The stamp duty holiday allows someone to pay no tax on the first £500,000 of a residential property they purchase. This has resulted in HMOs being in hot demand. Although landlords still have to pay the three per cent stamp duty charge, the temporary tax break can save investors thousands of pounds.

The second reason is that there are changes to planning laws. The government announced new planning laws for commercial property. This means that these properties can be converted into housing without full planning permission and as a result, HMOs are more accessible to commercial property owners.

According to the director of property lender MT Finance Tomer Aboody, auctions have been extremely busy with plenty of stock coming to the auction houses from investors looking to cash out of the market as it heats up, whilst experienced landlords have been looking for HMOs to add to their portfolios.

There are also additional costs to bear in mind with HMOs, but the financial model for HMOs is that extra income far exceeds costs incurred. As in any business, ‘think net profit’. There can also be tax advantages to investing in HMOs in that more of your costs might be tax deductible.

The rules to abide to

If you are a landlord and you are thinking about renting out your property as a house in multiple occupation in England or Wales, there are several rules you must abide by. Firstly you must contact your council if you need a license.

If you want to rent out your property as a house in multiple occupation in England or Wales you must contact your council to check if you need a licence.

You must have a licence if you’re renting out a large HMO in England or Wales. Your property is defined as a large HMO if all of the following apply:

- It is rented to 3 or more people who form more than 1 household

- Some or all tenants share toilet, bathroom or kitchen facilities

- At least 1 tenant pays rent (or their employer pays it for them)

Even if your property is smaller and rented to fewer people, you may still need a licence depending on the area, so check with your council if you are unsure.

A brief snapshot of the UK’s purpose-build student accommodation market

Despite Covid-19, international demand for UK student accommodation remains strong from students and investors alike. Investment in UK purpose-built student accommodation (PBSA) has grown dramatically in the last two years.

According to Savills Research, demand for student accommodation should be robust. The outlook for 2021 is considerably more positive, as demand for university places tend to rise when unemployment is higher. The UK’s 18-year- old population is now growing, following years of decline, while the participation rate continues to rise. This therefore means a growing pool of potential university applicants, with 97% of universities planning to teach courses in person in 2020/21.

Some key statistics

According to Savills, 60% of overseas students are more likely to live in PBSA than domestic students, and there has been a 24% annual increase in undergraduate applications from China.

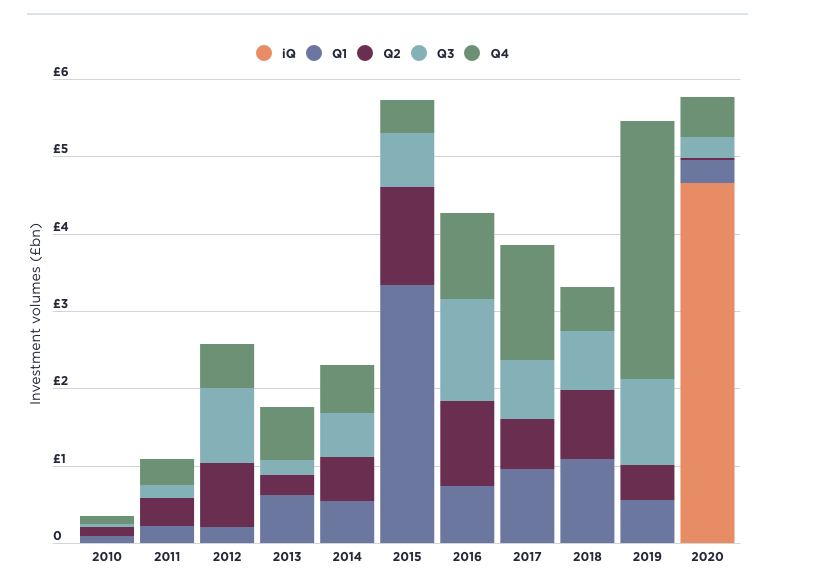

The graph below shows the investment flows into UK PBSA by quarter. As you can see from the graph below, with the exception of iQ, which completed in May, just two investors completed transactions in Q2. However, as vaccination programmes accelerate we are seeing growing investor confidence in the student accommodation sector and greater appetite for acquisition opportunities.

Investment flows into UK PBSA by quarter

(Source: Savills Research)

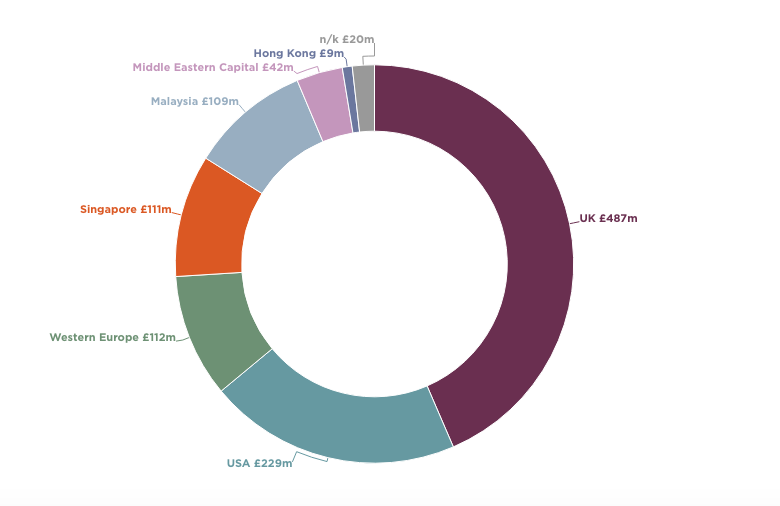

Below shows data regarding where exactly investments into the UK’s Purpose-Built Student Accommodation (PBSA) derived from. As you can observe the majority of the investment came from the UK, with £487 million being invested, second was the USA with a total of £229 million and other investments came from Western Europe, with £112 million being invested as well as Singapore, Malaysia, Middle Eastern Capital and Hong Kong

2020 Investment in UK PBSA by source of capital*

(Source: Savills Research)

On the right track

With the right systems and processes in place, there is no doubt that HMOs can make an excellent investment option, offering a yield that can’t be achieved with a traditional let and with the substantial amount of investments in the purpose-built student accommodation (PBSA), there is no doubt that both the HMO market and the PBSA market are now on the right track to withstand the pandemic and will go from strength to strength.

If you are looking to find a London spare room, studio flats to rent in London, rooms for rent, student accommodation or a flat for sharing on RoomforRent.rent.